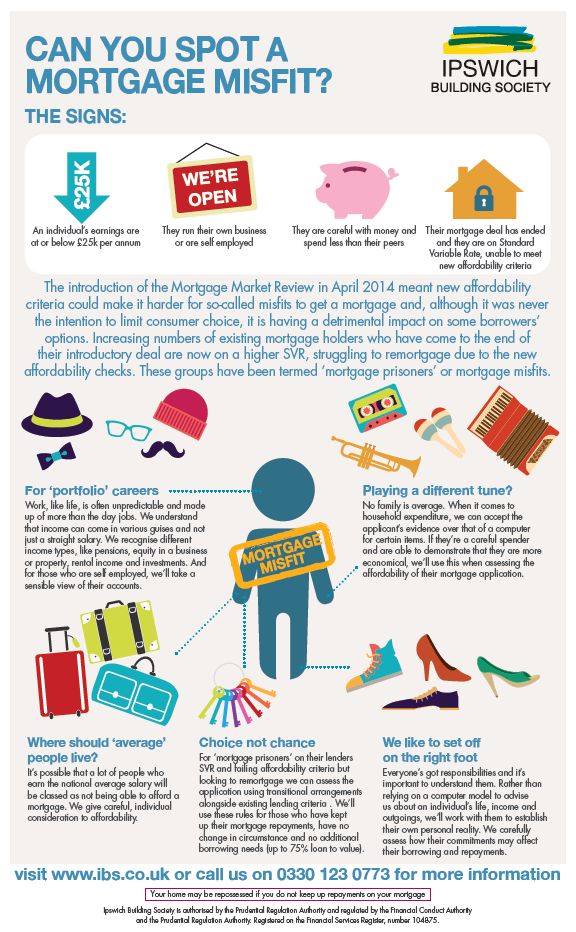

You may not realise it yet but you could be a mortgage prisoner, like tens of thousands of other homeowners across the country. You may be blissfully (well not quite blissfully) paying off your mortgage every month, completely unaware that when your mortgage deal comes to an close at the end of your 2, 5 of 10 year term, you may well be trapped on a higher Standard Variable Rate (SVR).

To explain why, we need to back track to last year.

The Mortgage Market Review

Last April, new mortgage rules were introduced under the formal banner of the Mortgage Market Review. In short this means that mortgage providers have stricter affordability checks than before: providers will look at an applicant’s spending habits in more detail than before and also check that they can afford their mortgage repayments should interest rates rise in the future.

Whilst this could be a fairly nerve-racking process for anyone applying for a mortgage, in reality, these checks are a good thing as providers need to ensure that home-owners are only taking on debt that they can afford in the future.

These affordability checks are also affecting existing mortgage holders too. When a home-owner’s mortgage deal comes to an end, they will usually shop around rather than remain on the default SVR. However many homeowners may fail the new affordability checks and therefore will struggle to access a competitive deal with a mortgage provider. Due to being trapped on a higher SVR and unable to shop around, this group has been branded ‘mortgage prisoners’.

Transitional arrangements

Somewhat ironically, mortgage prisoners who are stuck on a higher SVR are perhaps more vulnerable to future interest rate rises and the associated increase in monthly mortgage payments, than someone who can secure a new deal at a lower rate.

However, there is hope for mortgage prisoners. The new mortgage rules also include something called ‘transitional arrangements’. It doesn’t exactly roll off the tongue but the terms should have a favourable outcome for so called mortgage prisoners.

In short, providers no longer need to apply the affordability checks as long as the existing mortgage holder meets specific criteria. These criteria are:

- the existing mortgage holder does not want to borrow any additional funds

- the existing mortgage has kept up with their monthly repayments

- the existing mortgage holder’s circumstances have not changed

Good news so far but, and it’s a fairly big but, not all providers are applying these transitional arrangements. Some providers may simply not want to attract what it might consider to be a riskier customer base: research from EDM highlights that seven out of 10 mortgage brokers said lenders were now too risk averse following the introduction of the Mortgage Market Review. In more extreme circumstances, criticism has been levied at providers for purposefully misinterpreting the rules to keep customers on higher SVRs. Whichever is true, the Council of Mortgage Lender’s figures corroborate the fact that existing mortgage holders are struggling to get a new loan as the overall number of re-mortgages fell to its lowest level since 1997.

Manual vs. automated lending

Another factor in whether transitional arrangements are applied fairly is in relation to the type of underwriting that each provider undertakes. Some larger lenders only offer automated lending services, meaning that a computer-based system is in place which does not offer the flexibility to consider individual circumstances.

Manual underwriting is the exact opposite in that qualified professionals review applications on a case by case basis, to avoid a ‘computer says no’ response. The outcome of a manual lending approach is much more likely to be beneficial to mortgage prisoners who meet the criteria outlined above.

What if the homeowner’s circumstances have changed?

Life is full of unforeseen changes; the main priority is if these changes impact on the ability of a homeowner to continue to pay their mortgage. The use of transitional criteria enables a lender to review a homeowner’s current situation and decide if a new mortgage is affordable and in their best interests.

Given the numbers affected, it is quite likely that you, a friend or family member will be affected by this mortgage prisoner issue. However there are several providers, including Ipswich Building Society, who will promise to review mortgage applications on an individual basis, so you or they should not need to remain trapped on a high SVR.

Editor’s note: This post was brought to you in collaboration with Michelle Monck, General Manager of Marketing at the Ipswich Building Society. Ipswich Building Society has announced a new programmed of mortgage lending for borrowers who have been let down by other lenders as a result of stricter rules imposed in 2014 by the Mortgage Market Review (MMR).

YOUR HOME MAY BE REPOSSESSED IF YOU DO NOT KEEP UP WITH YOUR MORTGAGE REPAYMENTS

photo credit: Considering The Tax Shelter via photopin (license)

If you are a mortgage prisoner, please join my Facebook pressure group. Early days but I eventually hope it makes a difference to end this profiteering:

https://www.facebook.com/groups/324163371301670/