We trust banks to keep our money safe and look after basic stuff.

Like closing our loan account when debt is paid off. Transferring money when we purchase stuff and crediting our accounts when money goes in.

We trust banks not because we know what they do and how they do it. We trust them just like we trust water companies (naively, it turns out) because our lives will be impossible without ignorant trust.

But ignorant trust can be a colossal mistake. Banks, as you will see from our story, drop the ball.

Our bank did, and it was not pretty. When banks slip, it’s our pockets that take the hit—and trying to recoup those losses? It’s like squeezing water from a stone.

So, where does that leave us, the trusting patrons?

Please stick around and hear our cautionary tale. It may change the way you interact with your bank.

The Banking Blunder

Some of our long-term readers would recall that in early 2010, we had so much debt that I feared we might lose everything. Think that I am being dramatic? Probably a bit, but my drama was justified – we had £100,000 worth of consumer debt, which we paid off in exactly three years.

Our strategy was simple – earn a lot, spend little, and put the difference on the debt. Oh, and reduce the interest on the debt.

To reduce the interest, we went against traditional personal finance advice and took out a consolidation loan with our bank – with our house as the collateral.

This means that our bank gave us a loan at a much lower interest rate than credit cards but put a charge against our house. Failing to pay the loan would mean losing our house.

Scary as hell, right?

That is why we got our act together and paid off the loan in three years (instead of the agreed term of ten years). Our debt was paid off, the bank closed the loan account, and we were in a splendid financial position and ready to live happily ever after.

Or so we thought.

Several months ago, we decided to re-mortgage.

(Before anyone starts questioning that, we reduced the mortgage considerably and the new one is approximately 9% of the house’s value.)

All was moving smoothly. We have equity, we have income, and we have a positive cash flow. Everyone is happy, and John and I are preparing to exhale because another life management chore has been completed.

Until a message from the solicitor dropped in our mailboxes. It said:

“And what about the second mortgage on the house?”

Talking about being blindsided, I tell you.

After some digging, it turned out that our bank closed the loan account but never lifted the charge it placed on our house. So, the search still showed that our house is collateral for a loan.

Our bank should have removed the charge. It missed it for over ten years (we paid off our debt in February 2013) and would have continued to miss it if we were not re-mortgaging.

Next, We Found Banks Are Difficult to Pin Down for a Conversation

Photo by Icons8 Team on Unsplash

Panic. (Cost to our mental health.)

John rushed to our local branch. (Yes, we are lucky to have one still.)

He was given a form that didn’t appear to apply to our case.

Then he phoned the bank following the telephone system (cr*ppy music overload warning).

The bank official told him to fill in the form.

On the form, there was a field for the account number of the loan account. John asked the bank to provide it; they didn’t have it and couldn’t find it – which I found very disconcerting.

How We Sorted Out This Banking Mess?

Luckily, John keeps things – documentation, papers, books, clothes.

He found the loan account number, filled in the form, and finally found and talked to someone who understood what had happened.

After that, the bank was helpful. (Apart from asking for some of the information several times because, as we all know, the parts of an organisation do not necessarily talk to each other.)

A couple of weeks later, the charge on our house was lifted so that we could proceed with the new mortgage.

What did This Bank Mistake Cost?

This bank mistake cost us:

- A lot of worry and hassle.

- A two-week delay in progressing the new mortgage.

- Interest (we would have earned) of £126.

- Interest (we are paying our previous mortgage provider) – hypothetical because of uncertain completion date but could be substantial.

And this is the best case we managed to pull off.

Now, let’s think about what would have happened if John hadn’t kept over ten years old documents in his office (and I promised him, I would never bug him to clear his office ever again).

I suspect that lifting the charge against our house would have taken a very long time. Our new mortgage arrangement would have fallen through. Our costs would have been into the tens of thousands including fees we already paid, the much higher interest rates on our current mortgage and the time and effort needed to take our bank to the Ombudsman.

That is not negligible, and it is not innocent.

Our bank dropped the ball seriously by closing our loan account without lifting the charge on our house.

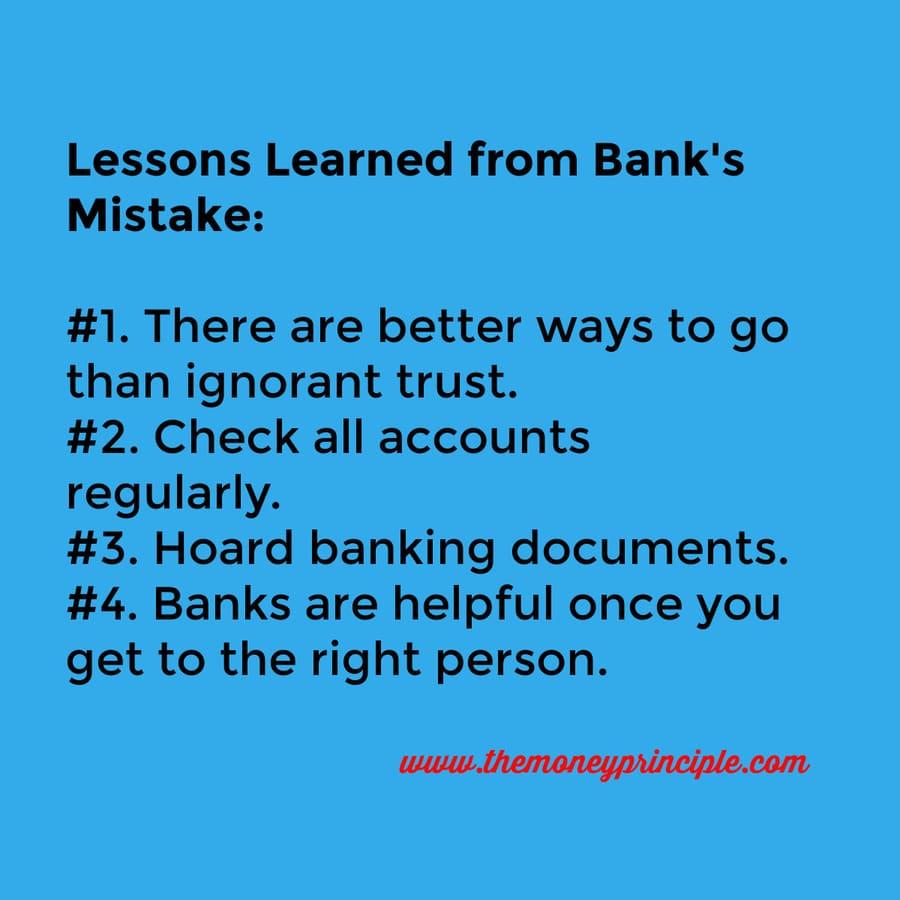

What Lessons We Learned from Our Bank’s Mistake?

Here are the lessons we learned through this misadventure:

- There are better ways to go than ignorant trust when it comes to banking.

- Check accounts regularly. This includes loan accounts with guarantee (or collateral).

- Keep banking documentation for a long time; you never know when you may need it.

- Banks can be helpful after you get to the person who knows about your problem.

Finally, Vigilance is Essential for Financial Health

We should have checked to ensure the charge against our home was lifted.

It isn’t our responsibility, true. But we are the ones who would have been burned by the bank’s mistake.

Don’t be like us.

Check your bank accounts – including any loan accounts, current and past- to ensure that all is as it should be.

Don’t delay! Do it now.

Photo by Bernard Hermant on Unsplash