Yesterday I opened my Nutmeg account (for my readers in the US, Nutmeg is the UK ‘sister’ of Betterment) and the first thing I saw was a message saying:

I’m in for the long run: history tells us that savvy investors stand firm when markets are choppy!

The next thing I noticed is that there is less money in my account than I’ve put in.

“This is no good” – I thought. “This means I’m losing my hard-earned cash.”

And you know what?

Smart investor or not, all I wanted to do is take my money out.

This is painful on too many levels.

Whenever I check my investment accounts at the moment, I feel the pain of:

- Loss of the money it had made;

- Loss of the money I had saved and invested; and

- Loss of my hope for an early and comfortable retirement.

Too much loss, you see. And I’m not a stranger to ‘loss aversion’ – this is the fear of loss which is, according to some studies, a much more powerful motivator than the hope of gain.

(I’m no economist and have absolutely no intention of becoming one. But ‘loss aversion’ is a very useful notion from behavioural economics encapsulating the tendency of people to prefer avoiding loss rather than expecting gains. Some studies show that the threat of loss is twice as powerful psychologically as the promise of gain.)

Well, I cannot avoid ‘loss aversion’ but I can resist succumbing to it.

If I succumb, I’ll cash my Nutmeg investments and cut my losses.

Many people have done that; many are pondering whether to do it and when.

I’ve decided to stick with it and here are the reasons why I still love Nutmeg enough to stay with them:

#1. What are the alternatives?

Seriously?

None. Apart from keeping my money under the mattress or in a saving account in the bank. Or I could have an ISA with another provider and get all of 0.8% annual interest. Which of course brings me back to keeping my money under the mattress.

I’m certainly not going back to spending all I earn because investing is a bit problematic.

#2. It is a matter of trust

Whether I decide to stay with Nutmeg or not is a matter of trust. I received several e-mail messages from readers who were so disappointed in the performance of their Nutmeg portfolio that they were considering pulling out. They also have lost their trust in Nutmeg.

I trust them. I was an early adopter of Nutmeg investing but not one who is blindly following the latest fashion – I research things, analyse them and discuss decisions with John (who is rather risk-averse and research-oriented).

Nutmeg is a solid company during very hard time for investors and markets.

#3. They did return rather well when markets were buoyant

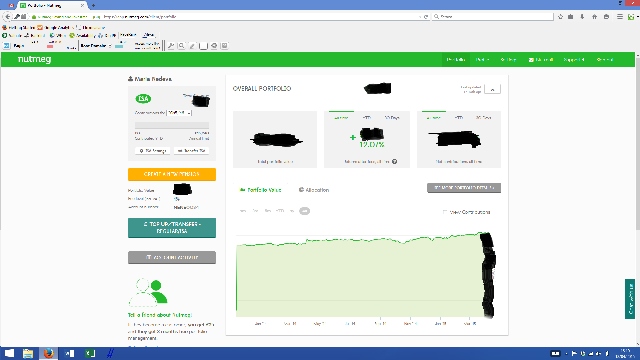

Did you notice something interesting in the picture?

This is a screenshot of my Nutmeg portfolio on 13 April 2015; it was returning over 12%. This lasted till August and since then my account has been going up and down so fast that it’s been giving me whiplash.

Apart from knee-jerk that is.

Still, the point is that Nutmeg was returning rather well when the markets were buoyant.

Hopefully, the market will recover. If not, we are back to my first point – what are the alternatives?

#4. They have lost but not as much as others

Okay. My account has lost but it is in line with other investments. My Nutmeg account is down by about 13% which means that I’m 0.46% under what I put in it.

This is life and at the moment life in stocks and shares is a bit tough.

#5. My account will recover

Well, not only mine really. This is an overall expectation at the moment.

Statistics is on our side, friends: over the last 100 years, the stock market has returned on average 10% annually. There has been only one decade when the return was negative – the one immediately preceding WWII.

I reckon if things are really that bad, my Nutmeg account – and staying with Nutmeg – may turn out to be a very small problem in a sea of misfortune. Now you see, why I’m betting that my Nutmeg account will recover.

#6. It is partially my fault

It is a matter of risk tolerance you see.

On Nutmeg you set the risk you are prepared to take. Risk is set between 1 (very, very low risk) and 10 (stupidly high risk).

Mine was set at 7; you see, this is a moderately reckless risk. In the ‘good times,’ my portfolio was doing well but when trouble struck it fell as fast as the body temperature of a marathon runner at the end of a race.

John, on the other hand, set his risk to 5 which is moderate. His portfolio is still 5.21% up.

Here we go! It is all about learning, isn’t it?

Finally…

It is tempting to call it a day at the moment but please don’t. Just remember that in the long run portfolios will recover and returns will go up again.

As for me, I may be tempted as well; I may be starting other investing experiments. But I still love Nutmeg financial enough to stay with them; and to add to my portfolio. One thing I did though is to change my risk level to 5. I will let you know what happens.

It seems like your thinking is right on base. You cannot expect to take zero risk and still get a reward like some readers that are mailing you. In the long run you will come out ahead! Those looking to make a quick buck probably deserve to lose a bit of money if they pull out for not understanding the basics of investing and risk vs. reward.

@Derek: I believe that there are two issues involved: a) people who want to make a ‘quick buck’; and b) people who need to draw on their investment (retiring, illness etc.) and have no choice but to do this at a very bad time. I agree with you about the first group and feel desparately sorry about the second one.

I have been wondering about Nutmeg, so I’m glad that you shared this post! I use Betterment and I am pretty happy with the results so far…am actually saving!

@Michelle: Great minds and all that :). Yes, we were early adopters when Nutmeg started and it is fine for part of our investments.

Hi Maria and thanks for this. Is it worth using nutmeg for a “just invest” account or is it only worth it for ISA stocks and share accounts? Thanks

@Jimmy: It will be worth it for general investing account as well (without the tax benefits that the ISA brings). Were I to open one of those, I’d be selecting the ‘fully managed’ option which is relatively low fees. I’d also be watching (particularly now that we should be expecting a bear market) the distribution between stocks and shares and bonds (will have up to 50% stocks and shares and the rest bonds and cash). But this is only me :).

“Only you” is the best advisor and source of financial knowledge I’ve had for years 🙂 Thanks!